In a sign that the stock market is forward looking, the S&P 500 Index returned 20.54% in the second quarter. This large return happened despite an almost complete shutdown of the economy due to coronavirus and one of the sharpest declines in GDP since the Great Depression of the 1930’s. Clients who followed our advice at the end of the first quarter and used the bear market in equities to buy stocks at depressed prices need to review their asset allocation. We recommend that most clients move equities back down to a neutral allocation and capture the gains from the second quarter.

The first half of 2020 has been one of the most volatile periods in U. S history both for the economy and the financial markets. Analysts are estimating that the U.S economy declined between 35% to 40% in the second quarter. The Administration, Congress and the Federal Reserve recognized the gravity of the economic crisis and all responded with unprecedented fiscal and monetary stimulus to revive the economy. The Federal Reserve has realized that the mere mention of policy change is enough to move the markets in a positive direction. This power to move the markets is why the adage “don’t fight the Fed” exists. It is simple and effective for the Fed to announce policy changes. The swift market reaction allows investors less time to take advantage of low prices. The S&P 500 went from 2,191.86 on March 23rd to 2,851 on April 14th. That was an increase of 30% over 16 business days and another example of why it is so hard to time the market. It is important to have a plan in place before the market drops to take advantage of mispriced securities. Having a select client base at Virtue Asset Management made it easier to adjust portfolios during stressful market times. This allowed us the time to identify and purchase mispriced securities including individual stocks, closed end bond funds and convertible preferred stocks.

The S&P 500 Index returned 20.54% for the second quarter and for the first half of the year returned -3.08%. Large Cap stocks continued to outperform other asset classes in the first half of the year. The S&P Mid-Cap Index returned 24.07% for the second quarter and has returned -12.78% for the first half of the year. The S&P Small Cap Index returned 21.94% for the second quarter and has returned -17.85% for the first half of the year.

U.S. Large Cap equities continue to outperform the rest of the world. International equities, as measured by the MSCI EAFE Index returned 14.90% for the second quarter and returned -11.37% for the first half of the year. Emerging markets, as measured by the MSCI Emerging Markets Index returned 17.93% for the second quarter and returned -10.01% for the first half of the year. Fixed income, as measured by the Barclays US Aggregate Bond Index returned 2.90% for the second quarter and returned 6.14% for the second half.

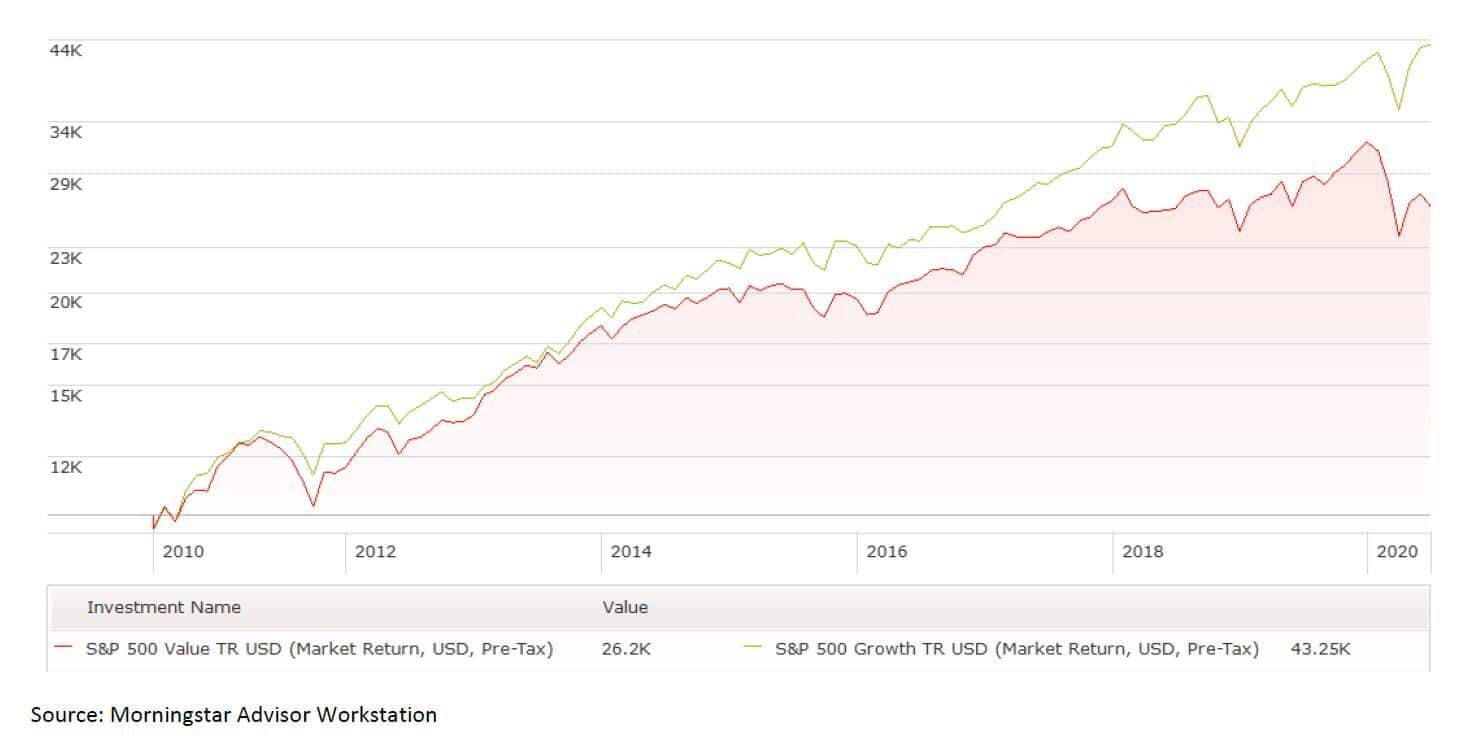

One theme that has continued throughout 2020 is the outperformance of growth versus value. Through the first half of the year the S&P 500 Growth Index returned 7.93% versus the S&P 500 Value Index which returned -15.52%. The S&P Growth Index has returned 16.62% per year over the last ten years. This return has significantly beat the S&P Value Index which has returned 10.88% per year. The price to earnings (P/E) ratio using the last fiscal year earnings for the S&P 500 Growth Index is 29.66 compared to 14.37 for the S&P Value Index.

Value of $10,000 Invested in Growth and Value Indexes 10 Years Ago

The S&P 500 Growth Index is dominated by technology companies that are the leaders in their industries. These companies enjoy limited competition and have projections for revenue and earnings increases greater than most companies in the S&P 500 index. We recommend owning many of these leading technology stocks including Apple, Facebook, Microsoft and Alphabet (Google), but we still think valuation matters for individual stocks and indexes.

One of the reasons growth stocks have performed well is the very low interest rate environment we have been in since 2009. A five-year U.S. Treasury bond currently yields .29%. When calculating future cash flows for companies, low interest rates mean that future dollars are worth almost the same as current dollars. As a result, investors are more willing to look at future earnings when valuing specific companies. Therefore, Uber can have a market capitalization over $50 billion despite never having a profitable quarter. Another example is Tesla, which has a market capitalization over $170 billion despite only having two profitable earning quarters since 2017. We find it unlikely that these companies would have their current valuations if interest rates were closer to the normal range of 4% to 6%. With normal interest rates, the present value of future earnings would be significantly reduced compared to current earnings. Despite the historically low interest rates, we are still cautious with some growth stocks. When you are focusing on earnings that far away in the future, one misstep can significantly change the earnings forecast. At Virtue Asset Management, we like to focus on companies that we think have a predictable earnings path. When you own high quality companies it should provide some level of comfort during a price decline and hopefully prevent people from panicking and selling at the bottom.

As we discussed at the end of the first quarter, without guidance on earnings, there is a wide range of possibilities for year-end targets. It seems likely that most industries will be able to operate at 100% in 2021. This has led most analysts to forecast S&P 500 Index 2021 earnings between $160 and $170. A major second wave from the coronavirus or a Democratic win in the White House and Senate are downside risks to earnings. If the Democrats gain control of the Presidency and Senate, there is an expectation they will raise corporate and individual tax rates. Higher corporate tax rates will lower the earnings for the S&P 500. However, with interest rates close to zero, we expect investors to return to a price to earnings (P/E) ratio near the ten-year average of approximately 20. This creates a 2021 year end range for the S&P 500 Index between 3200 and 3400. That will provide a return between 3% and 10% from the current level. This does compare favorably to bonds with interest rates near zero. Given the low interest rates we recommend that investors keep their stock exposure at the neutral point of their equity target range.