2026 First Quarter Market Commentary: Geopolitics, AI Execution, and the Path Ahead

The first quarter of 2026 has been a stark reminder that the market path is rarely a straight line. If you’ve been watching your portfolio lately, you’ve likely noticed a shift in momentum. After a period of relative calm, the S&P 500 declined 4.33% during the first three months of the year.

At Virtue Asset Management, we believe that understanding the “why” behind these moves is essential for staying the course. This quarter, markets were forced to adjust to a complex cocktail of rising short-term inflation expectations, intensified geopolitical tensions, specifically the conflict involving Iran, and a meaningful shift in the outlook for interest rates.

As an asset manager in Chicago, our job is to help you look past the daily headlines and focus on the structural changes happening in the economy. Whether you are looking for wealth management firms in Chicago or a local fiduciary financial advisor in Barrington, the goal remains the same: navigating uncertainty with a disciplined, long-term strategy.

The Macro Backdrop: Inflation and Energy Shocks

The primary driver of recent volatility has been the resurgence of near-term inflation concerns. Much of this is tied directly to energy prices. As geopolitical tensions in the Middle East escalated, oil prices followed suit, reigniting fears that inflation may prove stickier than previously hoped.

This has a direct impact on equity returns. Specifically, it reduces the likelihood that “price-to-earnings multiple expansion” (essentially, investors being willing to pay more for every dollar of company profit) will drive the market higher in the near term. Instead, we are entering a phase where actual earnings growth, the hard numbers, must do the heavy lifting.

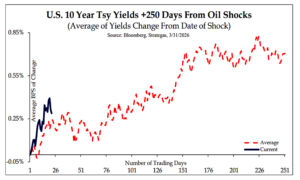

Interest Rates: The “No Cut” Reality

At the start of 2026, many market participants were pricing in two to three Federal Reserve rate cuts. Today, that expectation has shifted to essentially no cuts.

History shows us that following major oil shocks, U.S. 10-year Treasury yields have typically risen by approximately 70 basis points over the subsequent year. We are currently tracking a similar pattern. For you as an investor, this “higher-for-longer” environment creates a more challenging backdrop for stocks.

When rates rise, future earnings become less valuable today, which tends to compress valuation multiples. This environment favors businesses with strong current cash flows over those that rely heavily on the promise of future growth. If you are focused on tax-efficient investing in Chicago, this is a critical time to review how your fixed income and equity sleeves are interacting in a high-rate environment.

The 2026 Midterm Cycle: A Historical Perspective

It is also important to remember that we are in a midterm election year. Historically, these years present a more challenging backdrop for equities. In fact, March 2026 marked the worst S&P 500 performance in a midterm election year since 1942.

While the Iran conflict appears to have accelerated the typical four-year election cycle volatility by about four to six weeks, the pattern remains familiar. Sentiment can shift quickly when multiple risk factors converge. However, periods of market dislocation like this have historically created attractive long-term opportunities. As a fiduciary financial advisor in Chicago, we view these pullbacks as moments to selectively add to high-quality equities when the risk/reward profile aligns.

AI: Moving from Potential to Execution

Artificial Intelligence (AI) continues to be the dominant narrative, but the conversation is evolving. We are moving away from the “hype” phase and into the “execution” phase. Investors are no longer just looking for potential productivity gains; they are looking for realized profits.

The recent capital raise by OpenAI, valuing the company at approximately $800–$850 billion, underscores the massive scale of this opportunity. However, it also shows how much future growth is already “priced in.”

History provides a cautionary tale here. Netscape was the pioneer of the internet era, yet it ultimately lost its dominance as competition intensified. As AI becomes commoditized, we expect to see significant differentiation between companies with durable competitive advantages and those simply spending money without a clear path to revenue. This reinforces why we emphasize selectivity in mega-cap technology.

AI Disruption Across Sectors

We are also seeing AI influence other areas:

- Software: Traditional recurring revenue models are facing scrutiny as AI lowers the barriers to entry for new competitors.

- Private Credit: We are monitoring some areas of private credit where underlying business models may be disrupted, though we do not see broader systemic risk at this time.

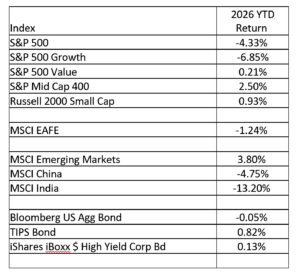

Quarterly Performance Summary

Performance across asset classes was broadly negative in Q1, with value-oriented and mid-cap stocks showing more resilience than growth-heavy indices.

Why the Long-Term Outlook Remains Constructive

Despite the headlines, there are reasons for optimism.

- Consumer Support: Tax refunds increased at a 19% year-over-year rate in March, which could provide a cushion for consumer spending.

- Trade Dynamics: Effective tariff rates have declined from roughly 11% to 8% over the last five months, potentially offsetting some inflationary pressure.

- Valuations: The S&P 500 is currently trading at roughly 20.5x forward earnings, which is actually slightly below the 10-year average of 21.76x.

If earnings expectations are met and valuations revert toward historical averages, we see a target of approximately 6,920 for the S&P 500, representing about 6% upside from current levels.

The Virtue Approach: Local Expertise for Global Markets

Navigating these markets requires more than just an index fund; it requires a fiduciary who understands your specific goals. Whether we are discussing your portfolio in our new Barrington office or reviewing your business planning needs, our focus is on providing clarity in an increasingly uncertain environment.

We continue to favor U.S. equities over international markets, supported by stronger innovation and a more favorable regulatory environment. While the near-term risk remains skewed to the downside due to geopolitics and interest rates, we believe the long-term drivers of productivity, led by AI and technological advancement, remain intact.

If you are concerned about how the recent market dip impacts your retirement timeline or want to discuss tax-efficient investing in Chicago, we are here to help.

Contact Virtue Asset Management today to schedule a portfolio review and ensure your strategy is built for the volatility of 2026.

Disclosures

Investing involves risk, including the possible loss of principal and fluctuation of value. Past performance is no guarantee of future results.

This letter is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date noted above and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Virtue Asset Management, LLC, to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Virtue Asset Management its principals, employees, agents or affiliates. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will materialize. Reliance upon information in this post is at the sole discretion of the reader.

Please consult with your Virtue Asset Management financial advisor to ensure that any contemplated transaction in any securities mentioned in this letter aligns with your overall investment goals, objectives and tolerance for risk. In addition, please note that Virtue Asset Management, including its principals, employees, agents, affiliates and advisory clients, may have positions in one or more of the securities discussed in this communication or effect transactions contrary to the views expressed in this communication based upon individual or firm circumstances. Any decision to effect transactions in the securities discussed within this communication should be balanced against the potential conflict of interest that Virtue Asset Management has by virtue of its investment in one or more of these securities.

Additional information about Virtue Asset Management is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary (Form CRS), which are available online via the SEC’s Investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov/firm/summary/283438.

Virtue Asset Management is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting or tax advice. Virtue Asset Management does not provide investment banking services nor engages in principal or agency cross transactions.